RBIG Broking Director Geoff Gregory looks at how economic uncertainty and the cost-of-living crisis could create fresh business risks and impact commercial insurance cover.

Here he examines the challenges which may arise and how business owners and managers can better protect their buildings, assets and operational continuity.

Overview

The UK economy continues to face turbulent times. Interest rates are rising as the Bank of England deploys one of the few tools available to it in order to combat double-digit inflation

Fast-rising costs and uncertainties over the future supply of energy are another major concern for business leaders. The recent fall in value of the pound has only exacerbated those worries.

Many also cite Brexit-related challenges which they report are stifling growth.

In November 2022 the Office for Budget Responsibility declared that the UK economy had entered recession and that unemployment would rise by 500,000.

Simultaneously, business confidence collapsed.

The outlook is more than uncertain.

Business impact

These factors and the real prospect of protracted economic contraction will impact businesses in a variety of ways.

There will inevitably be pressure to deliver greater cost efficiencies, across the board but with energy and fuel consumption high on the priority list.

At the same time, increased demands may be placed on payroll as employees look to soften the blow of soaring inflation. Simultaneously potential recruits may take advantage of a labour market that favours them.

Whilst recessions are typically marked by higher unemployment rates, this is not currently true in the UK. Whilst the number of vacancies had fallen by the beginning of Q3, data released in October 2022 by the Office for National Statistics nonetheless reported some 1.25 million posts remained unfilled.

The number of unemployed people per vacancy fell to the lowest level ever recorded. This illustrates just how much more competitive the recruitment market has become, potentially impacting productivity and payroll costs.

Social impact

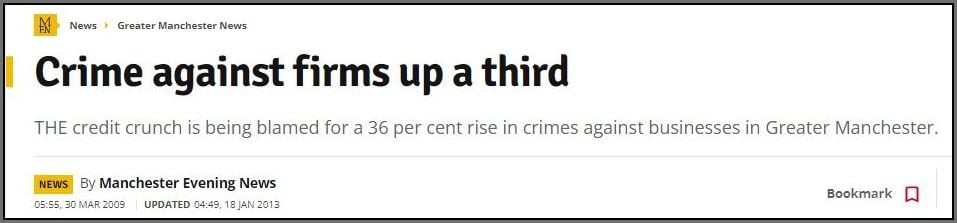

There may be social impacts too. Whilst it’s important not to confuse correlation with causation, it is not unreasonable to anticipate a rise in financial and property crime whilst the economy is in recession.

We’ve seen it before.

Following the global financial crash in 2008, insurer Axa reported a 36% increase in crimes against Greater Manchester businesses. The rise, it said, was “typical in a recession.”

This may all sound depressing. However, action can be taken to mitigate against the various recessionary impacts on business. There are also things to watch out for should you be thinking of implementing new policies and procedures in order to minimise costs and maximise efficiency.

Commercial Property

There is a potential for increased risk to both property and contents. Following the 2008 crash, Axa reported malicious damage to property rose by 14pc and arson attacks by 23%.

Whilst the targeting of unoccupied failed businesses was clearly a factor, it is nonetheless prudent to ensure your property is adequately protected, both physically and through appropriate and effective commercial property insurance.

Significant increases in the price of construction materials are also impacting reinstatement and rebuilding costs. In May 2022, the Royal Institute of Chartered Surveyor’s (RICS) Building Cost Information Service’s General Building Cost Index had increased by 13.1% against the previous year. Some materials recorded much greater increases, with steel up by between 50%-70%, timber and roofing by 50%*, concrete 20% and bricks 12%.

Action points

- Review existing security systems and protocols. If you are able to increase protection, please advise your RBIG account manager who can update your insurer. This may assist in minimising your renewal.

- If you have to rationalise your business and close offices, warehouses or other property, consider taking extra security precautions. The same is true should you need mothball construction. projects. In 2009 thefts of plant and machinery from building sites increased. Always advise RBIG or your insurer if you vacate, leave your premises/building or have an unoccupied site.

- Review your existing commercial property insurance. Aside from rebuilding costs, here are a number of things you should consider such as any variation in stock levels, plant and machinery inventory and value. Such factors can impact both the validity or extent of insurer liability and your renewal premium.

Fuel & Energy

You don’t need us to tell you that the price of petrol, diesel, heating oil, liquid propane gas (LPG), liquid natural gas (LNG) and electricity have all soared. Further rises seem inevitable given the international political landscape.

As such, businesses like yours are under even greater pressure to minimise energy and fuel usage and maximise efficiency.

We are aware, for instance, that some companies are switching from fixed to portable heating solutions in order to provide localised heat in line with workplace demand.

Whilst this may make practical sense, it’s important to take into account any insurance implications. For example, many commercial insurance policies many commercial insurance policies have exclusions for use of portable heaters which may result in claims not being covered by the insurer.

There are positive actions that may be taken to reduce fleet fuel use. Whilst there has been much recent hype about so-called “hypermiling”, the techniques championed are well established.

These are embedded in professional “defensive”, “eco” and “fuel efficient” driving courses.

Government data demonstrates how driving habits can return significant fuel efficiencies. Driving at a steady 50mph, rather than 70mph, can improve fuel economy by around 25%.

The Energy Saving Trust (EST) reports that “applied thoroughly and consistently [EST full efficient driving techniques], might save an average of around 15% and a realistic long-term goal for a fleet might be between 3 - 6%.”

Action points

- If revising your heating provision, ensure replacement appliances are covered by your commercial property insurance. If you will need store fuels on site, confirm this does not compromise your cover. Your RBIG account manager can advise and update your insurer.

- If operating a vehicle fleet, consider putting your drivers through a driving course. Defensive driving can not only help minimise fuel usage but, because they teach drivers to anticipate traffic flows and hazards, also reduce accident risk. Completion of an insurer-recognised course may help reduce your fleet insurance premium.

- Review eco-friendly driving techniques and their impact by reading the Energy Savings Trust’s guide, Advising fuel efficient driving techniques for your fleet. If you would like a copy, please ask your RBIG account manager or email [email protected].

- Consider the benefits of installing video telematic systems and/or fleet tracking solutions that provide real time data on driver performance. These technologies are championed by insurers as they contribute towards reducing accident frequency, provide tracking in the event of a vehicle theft and may offer additional cost benefits by reducing fleet operating costs.

Power Outages

For the first time in decades the UK is potentially facing planned power outages.

Whilst optimistic that we will not suffer winter power losses, the National Grid has nonetheless been preparing for the possibility of “rota disconnection”; three-hour scheduled power cuts.

It is important that your business considers how to minimise the impact of power loss across all its operations.

This should include:

- Alternative power sources – if you have or are considering deploying an emergency generator, ensure it is safely installed and sited and that you maintain adequate fuel supplies. Carry out a risk assessment.

- Equipment – ensure your equipment is correctly maintained and serviced as this may increase resilience. Consider how safety or operationally critical equipment may be impacted and the steps you need take in advance of any outage. Use surge protection to protect electrical devices. Ensure staff are appropriately trained and familiar with the correct equipment shutdown and restart procedures.

- Fire, security and access systems – Most fire and intruder alarms should have enough stored battery power to last a three-hour power cut, but you should check with your provider. You should do the same if you depend on off-site signalling. Remember too that your systems may rely on other facilities, such as lighting and security cameras, to operate effectively.

- If you have electrical pump fire sprinklers, review what you need do in case of power loss.

- If you deploy access control, consider how their temporary failure to operate may enable theft and/or cause safety issues.

- Heating – see Fuel & Energy section.

- IT and telecommunications – ensure data is protected through appropriate back-up systems. Plan for the possible loss of internet-enabled and mobile communications. Consider how you can best trade and communicate both internally and externally if your IT and communications networks go down.

- Lighting – Regularly test emergency lighting systems and distribute battery-powered torches and lanterns. Consider if the loss of your standard lighting will create any new or increased safety risks, how you may mitigate against them and minimise your potential exposure to employee and/or public liability claims.

This list is far from exhaustive but should give you an indication of the kinds of things you should consider. The insurer Axa has produced a useful Power Outage guidance booklet. If you would like a copy, please email RBIG's Simon Mannion.

The National Grid has also published a guide, Helping your business prepare for a power cut, which you can download here.

Cyber Security

Virtual Private Network specialist Surfshark, reports that in the year following the 2008 financial crash financial losses from cyber crime rose by 115%.

Data recently released by the company also revealed that for two consecutive years, the UK has topped the global cybercrime density list. The number of victims has grown by 40% since 2020.

The Department for Digital, Culture, Media and Sport’s Cyber Security Breaches Survey 2022 reports that in the previous year 39% of UK businesses identified a cyber attack. Of those attacks, 21% involved use of sophisticated targeting techniques such as ransomware, malware and denial of service.

In addition, in the wake of the invasion of Ukraine, the National Cyber Security Centre (NCSC) has cautioned of a “potentially protracted period of heightened cyber threat from Russia.”

The NCSC has warned against corporate complacency and published new guidance on maintaining strengthened cyber security during an extended period of threat.

The cost of a cyber attack can be immense, causing business interruption, reputational damage and direct financial loss.

Research published by IBM in 2022 found that, on average, a data breach cost the $4.24m and took 287 days to be identified and contained. Costs were significantly mitigated by a mature “zero trust” policy.

Action points

- Review your current cyber security protocols, taking into account NCSC’s guidance, Action to take when the cyber threat is heightened and subsequent advisory, Maintaining a sustainable strengthened cyber security posture.

The organisation has also published a handy Cyber Security Toolkit for Boards. - Review your insurance protections. Whilst some commercial insurance and liability policies offer cover for certain regulatory breaches, to fully protect your business from cyber-specific risks, you will need dedicated cyber insurance.

If you already have cyber insurance, ensure that you continue to meet underwriting requirements and that you are fully aware of limits and exclusions.

- Read our free guide, Cyber Insurance in the Age of Digital Dependence.

Client Failure

Whilst your business may be in good financial health, it may nonetheless be adversely affected by the collapse of customer.

With government Covid protections removed and the UK economy being marked by volatility and fragility, insolvencies are rising fast.

Insolvency Service statistics show that in October 2022 the number of registered company insolvencies had soared by 38% year-on year. That figure was 32% higher than it was in 2019, pre-pandemic.

The impact of corporate failures ripple down the supply chain, leaving out of pocket those for whom the failed business was a client.

Companies can insulate themselves from this risk by taking out trade credit insurance. This protects against the late or non-payment of debts, in turn helping maintain a health cashflow and guarding credit ratings.

Credit insurers can also assist policyholders in more effectively managing their risk, by proactively monitoring the financial health of their customers.

The Association of British Insurers reported in January 2020 that trade credit insurance helped UK businesses mitigate the impact of record-breaking bad debt. It found that the average value of claims had soared by 200%, reaching an historic high of £67,500.

Action points

- Ensure your credit control procedures are responsive and effective. Constantly review settlement of invoices, flagging any customers which delay payment.

- If you do not already have and/or are unaware of the benefits of trade credit insurance, request a copy of our free guide from your RBIG account manager or by emailing [email protected].

- If you do have trade credit insurance, ensure you advise your insurer of any change in the risk profile of your clients or your own business activities. You can discuss what may or not be pertinent to your cover with your RBIG account manager.

Employee Theft & Fraud

Following the “credit crunch” thefts from offices and workplaces rose by 10%. Police figures showed that in 2008 employees committed nearly 321,000 crimes against employers.

Theft by employees can range from the “petty” – stationery and low value office consumables – through to computing equipment, machinery and high-value fraud. All are likely to increase during an economic downturn as employees feel the financial squeeze and may relax their moral codes.

In 2009, the Fraud Advisory Panel noted that “The risk of fraud to businesses is at its greatest in times of economic downturn. Big companies can be badly shaken by fraud; small ones can be destroyed. Fraud prevention is an essential part of any recession survival strategy.”

Employee theft can take a number of forms. During a downturn employees may be more susceptible to criminal enticements to share confidential data or intellectual property. Alternatively, in response to deteriorating household finances, they may be more likely to steal physical property to convert into cash.

Action points

- Consider which areas of your business are most vulnerable to theft or fraud. These might include the physical – warehoused stock, office equipment – and your financial protocols and process – expenses, sales and purchasing. Ensure these are effectively monitored and policed and that your staff are fully aware of procedures.

- If possible, give a senior member of staff responsibility for monitoring, managing and addressing risk.

- Review the physical security of your premises. If you introduce additional protections, advise your RBIG account manager as this may assist negotiation of your commercial insurance renewal.

- Review your insurance covers. You may wish to take dedicated Employee Theft/Employee Dishonesty insurance. You can discuss your options with your RBIG account manager.

External Crime

As previously noted, crime rates tend to increase during economic downturns.

Insurer Axa noted the 2008 credit crunch coincided with a significant rise in crimes committed against Greater Manchester businesses. Cases of breaking and entering rose by 13 percent, vandalism 14% and arson 23%.

It is important to review your security arrangements in the light of potentially increased risk.

This should include confirming the effectiveness of your physical protections – such as intruder and fire alarms, CCTV, locks – and security patrols which are deployed to protect buildings, office equipment, machinery and vehicles. You should also review your IT infrastructure, mobile devices and cyber security protocols.

You should take into account any changes to the way your business operates in terms of systems, procedures and premises. Be mindful of external factors which could affect your operations. This might include neighbouring premises becoming vacant and a potential target for vandalism or arson. Whilst those premises may not be your responsibility, a serious incident may impact your premises and/or business activities.

If you handle cash, be mindful of the potentially increased risk of a planned or opportunistic raid, on site or in transit.

Business Interruption

Consideration should be given to the indemnity period incorporated within your business interruption cover. This should be examined in relation to the time it may now take for your business to fully restore operations following an insured incident.

A number of factors may impact the lead time necessary to reinstate commercial property, machinery, stock and other assets.

These include supply chain issues which could delay delivery of materials and parts and labour shortages.

Cover limits should also be examined in light of ongoing inflationary pressures, bearing in mind that these differ across industries and sectors within them.

Provisional data published in October 2022 by the Department for Business, Energy & Industrial Strategy shows that construction material prices had risen by nearly 17%, year-on year. This will clearly impact reinstatement costs.

Employers’ Liability

As the recession bites and rising energy costs hit the bottom line you may look to restructure your business operations.

This may involve redundancies, redeployment, amending shift patterns, altering hours of operation or other acts designed to lower costs and/or enhance efficiencies. Such actions may result in an increase in disputes which in turn trigger employers’ liability claims.

When considering any operational changes, be sure to maintain adherence to health and safety and employment regulations. For example, ensure that any changes to an employee’s role or responsibility are supported by relevant training and certifications.

It is similarly important to conduct risk assessments prior to instituting changes to the way your business and its employees operate.

If you plan to make a role redundant or to change the hours or responsibilities relating to it, carefully consider how you propose to do so. Be mindful of relevant employment legislation, not just in terms of statutory processes, but regulations designed to prevent discrimination.

Concerned? We can help

Whilst extensive, this is not an exhaustive list of the potentially increased risks your business may face in these economically volatile times.

Nonetheless, we appreciate that the issues raised and actions recommended here may prove daunting to time-pressed directors and managers.

We’re here to help. With more than 40 years’ service to the business community, we’ve seen and steered our clients through many challenging times. We ready to do so again, for you.

If you would like any advice or assistance in assessing risk or reviewing your business covers, we will be happy to help. Simply contact RBIG's Simon Mannion via email or calling 0161 304 5037 to arrange an on-site, telephone or video consultation.

If you have an enquiry specific to Trade Credit Insurance - which protects against late and non-payment - please email Dave Sterlini or call him on 0161 304 5056.